The 4% Rule Has a Cash Flow Problem

The Retirement Math Most People Avoid

For years, the retirement industry has pushed a simple idea: save a big pile of money, withdraw a small percentage every year, and hope it lasts.

That is the basic idea behind the 4% rule.

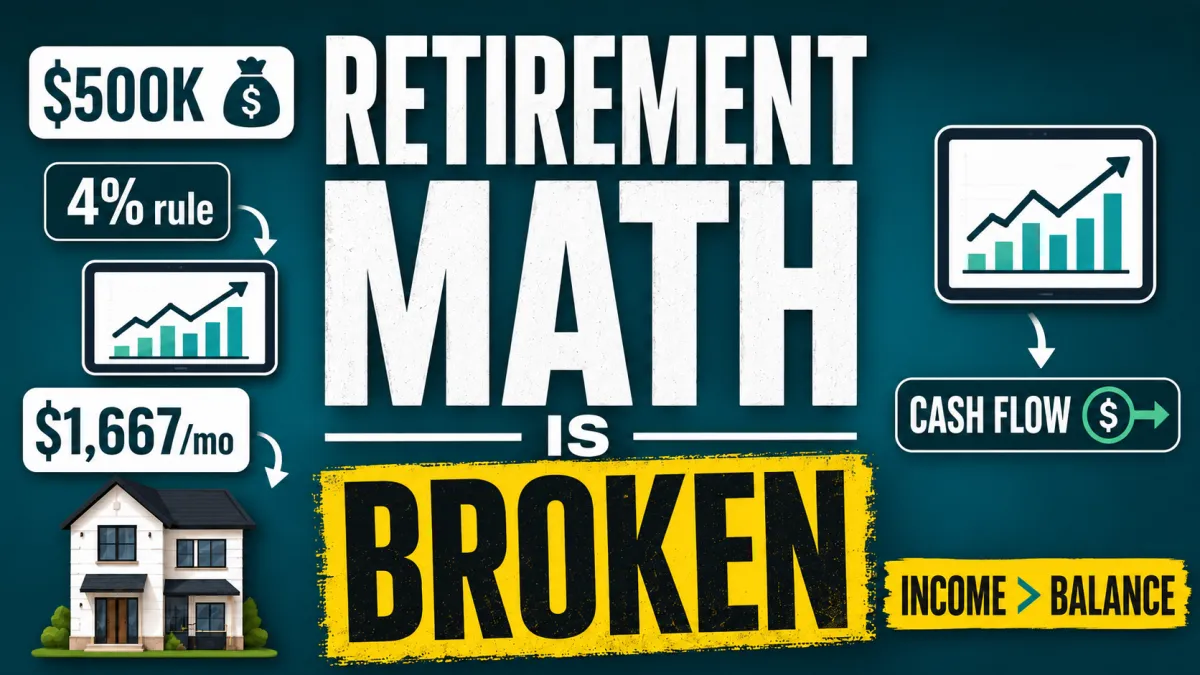

The 4% rule says that, in retirement, you may be able to withdraw about 4% of your retirement savings each year to help replace income. So, if you have $500,000 saved, 4% gives you $20,000 per year.

That sounds decent until you do the real math.

$20,000 per year is only about $1,667 per month.

Now add Social Security. Let’s assume Social Security provides $30,000 per year. That is another $2,500 per month.

Together, that gives you about $50,000 per year, or roughly $4,167 per month before taxes, inflation, medical costs, housing costs, vehicle costs, family needs, and life happening.

For some people, that may work. For many Gen X families, it is going to feel tight.

And here is the part Wall Street does not like to talk about: the 4% rule is built around withdrawing from a pile.

That means every month you are taking money out of the bucket.

Real estate, when positioned correctly, changes the question entirely.

Instead of asking, “How much can I withdraw from my pile?”

You begin asking, “How much monthly income can my assets produce?”

That is the difference between the Consumer Economy and the Investor Economy.

Consumers chase balances.

Operators build systems.

If you are considering how property fits into your bigger retirement picture, this article on real estate in retirement plans breaks down the difference between owning real estate personally and holding real estate inside a retirement account.

The Big Secret: Income Is the Real Asset

Most people think a $500,000 account is the asset.

I disagree.

The real asset is the income that account can produce.

If $500,000 produces $20,000 per year under the 4% rule, then the income value of that account is $1,667 per month.

That is the number we need to focus on.

Not the giant headline number.

Not the retirement calculator fantasy.

Not the brochure showing some smiling couple walking on the beach.

The real question is this:

What asset can produce $1,667 per month in dependable cash flow?

Because if you can build real estate income of $1,667 per month, you have created the cash flow equivalent of a $500,000 retirement account using the 4% withdrawal concept.

Now, does that mean real estate is exactly the same as a retirement account?

No. Do not be lazy with the math.

Real estate has repairs, vacancy, management, taxes, insurance, financing, tenant risk, market cycles, legal compliance, and operational headaches. This is not magic money.

But that is also the opportunity.

Because real estate is not just a paper account. It is a controllable asset when you understand acquisition, capital, and management.

That is what I call theOne Door Control System.

The $1 Million Question

Let’s take the math further.

If $500,000 at 4% equals $20,000 per year, then $1,000,000 at 4% equals $40,000 per year.

That is about$3,333 per month.

So when someone says, “I need a million dollars to retire,” what they may really mean is:

“I need around $3,333 per month of additional income.”

That is a very different problem.

Saving $1,000,000 can feel impossible for a 50-year-old who has raised kids, paid bills, survived recessions, watched inflation eat purchasing power, and maybe did not start early enough.

But building toward $3,333 per month in real estate cash flow?

That is still hard, but it is a different kind of hard.

It is not passive at first.

It is not overnight.

It is not guru hype.

It is not “buy one house and become rich by Tuesday.”

It is system-building.

It is learning how to acquire the right property, fund the deal correctly, manage the asset responsibly, and stack cash flow over time.

That is the ant philosophy.

The ant does not wait for perfect conditions.

The ant does not complain about the economy.

The ant does not spend all summer watching webinars and calling it progress.

The ant works the system daily.

Why Gen X Needs To Wake Up

Gen X is in a tough spot.

Many are too young to stop working, but too old to pretend time is unlimited.

A lot of Gen X men are looking at their retirement accounts and realizing the math is not as comfortable as they hoped. They have worked hard, stayed responsible, raised families, paid mortgages, helped kids, and carried the weight.

But now the clock is louder.

And here is where people get trapped.

They think their only options are:

Save more.

Spend less.

Work longer.

Hope the market performs.

Wait for Social Security.

That is Consumer Economy thinking.

It is defensive.

It is fearful.

It depends too much on outside forces.

The Investor Economy asks a better question:

What assets can I control that produce income whether I clock in or not?

That is where real estate deserves serious consideration.

Not because real estate is perfect. It is not.

But because real estate gives you something your 401(k) usually does not give you: a chance to influence the outcome.

You can improve the property.

You can negotiate the purchase.

You can change management.

You can restructure debt.

You can increase income.

You can reduce waste.

You can reposition the asset.

You can create forced appreciation.

That is control.

And control matters.

For a deeper look at the mindset side of this, read No One Is Coming To Save Your Retirement, where I break down why personal responsibility, cash flow, and action matter more than waiting for someone else to fix the future.

A.L.I.E.: The Simple Test

In GET UNBROKE, I talk about a simple concept:

Assets put money in your pocket. Liabilities take money out.

That is A.L.I.E.

A lot of people call things assets that are not really helping them.

A car is not an income asset.

A boat is not an income asset.

A bigger lifestyle is not an income asset.

A primary residence may build equity, but it does not pay your grocery bill unless you sell, refinance, or rent part of it.

Cash-flow real estate is different when purchased and managed correctly.

A rental property can produce income.

That income can help offset the pressure of retirement savings.

The goal is not to worship real estate. The goal is to build a machine.

A machine that creates monthly cash flow.

That machine may include long-term rentals, small multifamily, lease purchase strategies, private lending, property management efficiencies, or other real estate-backed income systems.

But the principle is the same:

Stop thinking only about the pile.

Start thinking about the pipe.

A pile gets spent down.

A pipe keeps flowing.

This is why I believe investors should think more about cash flow over appreciation instead of chasing properties that only look good on paper.

The Real Math

Let’s keep this simple.

A $500,000 retirement account at 4% produces:

$20,000 per year

$1,667 per month

A $1,000,000 retirement account at 4% produces:

$40,000 per year

$3,333 per month

So now we can reverse engineer the goal.

Instead of saying:

“I need $1,000,000.”

Say:

“I need to build $3,333 per month in durable cash flow.”

That could come from one property, several properties, a small multifamily, a lease purchase portfolio, real estate notes, or a combination of real estate income streams.

But do not get cute.

The numbers have to work.

You need reserves.

You need realistic vacancy assumptions.

You need repairs budgeted.

You need insurance reviewed.

You need taxes considered.

You need debt structured properly.

You need management that does not leak money.

Bad real estate is not an asset.

Bad real estate is a job with debt attached to it.

Good real estate is designed.

That is why I teach systems.

This is why serious investors need to focus on building deals that actually work, not just chasing the cheapest price or the prettiest property.

The Fear Problem

Here is what stops most people.

It is not math.

It is fear.

Fear of making a mistake.

Fear of tenants.

Fear of repairs.

Fear of debt.

Fear of looking foolish.

Fear of not knowing enough.

Fear of starting too late.

I understand that. Real estate has real risks.

But fear without action becomes expensive.

At some point, you have to decide whether you are going to remain a Consumer or become an Operator.

Consumers wait until they feel ready.

Operators get educated, run the numbers, build reserves, seek counsel, and move strategically.

The people who win are not reckless. They are not gamblers. They are not guru junkies.

They are steady.

They understand that wealth is not built by one dramatic move. Wealth is built by daily, unsexy, persistent compounding.

Like the ant.

Where Get UNBROKE Comes In

This is exactly why I wroteGET UNBROKE.

Not to sell you a fantasy.

Not to tell you to quit your job and buy ten houses by Friday.

Not to hype you up with millionaire nonsense.

I wrote it because too many good people are stuck in a financial system that trained them to consume, borrow, hope, and wait.

And waiting is not a strategy.

GET UNBROKE helps you rethink your relationship with money, cash flow, assets, liabilities, and real estate.

It is for the person who knows something has to change, but does not want another fake guru sales pitch.

It is practical.

It is direct.

It is a wake-up call.

Because the truth is simple:

You may not have time to save your way to freedom.

But you may still have time to build income.

That is the move.

Build the machine.

Control the asset.

Create the cash flow.

Fund life one door at a time.

Get the book here:

👉 https://a.co/d/0eMwJPKn

And when you are ready to talk through what one smart real estate move could look like, schedule a call:

👉 https://christensenproperties.com/call